Berkshire Hathaway 2018 Valuation

My clients and I have been owners of Berkshire Hathaway for a few years. Berkshire is a solid, relatively unlevered, well-managed, diversified, and highly tax-efficient investment. These factors make me comfortable owning a chunk of it even though the future returns are unlikely to be much more than 10% annualized.

In this post I’m going to walk through a conservative valuation of the different parts of Berkshire. In a later post, I’ll examine the growth in value over time and offer some broader thoughts on Berkshire’s current attractiveness.

If you click on this link, you can download my model. It will make it easier to follow along and you can also change some of the inputs and assumptions if you have different expectations than I do.

Valuation - Some Overarching Thoughts

I want to give you my assumptions up front. Valuing Berkshire is a big project, and to the extent that people tend to disagree, I think sometimes it’s because the assumptions on what is being done are wildly different. If you disagree with any of the results, it makes sense to come back to these assumptions.

First and foremost, I’m trying to look at the values of each individual business based on the cash flows. I will not be using industry comps. I will not be adding up assets. I will be looking at cash flow and attempting to discount those cash flows at an appropriate rate to find a value for the company.

Second, I’m valuing each of these businesses on the assumption that they pay out all excess cash flow. In reality the success of Berkshire, or any other business, depends to a huge extent on how management deploys future earnings. For this post, I will ignore that by saying that all of the earnings are paid out as a dividend, which doesn’t assign any benefit (or harm) for future good (or bad) capital allocation decisions. I’ll discuss my thoughts on whether future capital allocation is likely to hurt or help results in the next post.

Third, I use a 10% discount rate for Berkshire. If I can make 10% after tax with all of the advantages that Berkshire offers then I’m happy. Obviously, feel free to adjust the numbers with your own discount rate.

Valuation - Operating Businesses

I find it easiest to look at these businesses as four different entities - equity method investees, Burlington Northern Santa Fe, Berkshire Hathaway Energy, and Manufacturing, Service, and Retailing. The accounting and economic considerations are quite different for each of these, so it makes sense to me to value them separately.

Equity Method Investments

This is the smallest of the buckets and consists of Kraft Heinz, Berkadia, Pilot Flying J, and Electric Transmission Texas. I’ll include Kraft Heinz in the stock portfolio, so for this segment I’ll just include the other businesses. From p. K-80 of the 10-K, we see that these companies earned $563 million for Berkshire. We don’t have any other information about them, so I’ll just attach a 15x earnings multiple and say that these businesses are worth roughly $8.4 billion.

Berkshire Hathaway Energy

Berkshire Hathaway Energy consists mainly of a few large utilities across the US. BHE is 90.9% owned by Berkshire and earned $2.62 billion on $29.59 billion of equity in 2018. There are a few different ways to value this, but I’m going to use a simple one. Utilities are generally allowed to earn a 10% after tax return on their equity, and if you go back through old financials you’ll see that Berkshire has tended to earn ~10% ROE. Since I’m using a 10% discount rate and Berkshire is permitted to earn a 10% ROE, I’ll value BHE right at book value. Berkshire’s 90.9% interest of $29.59 billion in book value is $26.9 billion.

BHE also has a fairly large real estate brokerage business earning ~$200 million pre-tax. I’ll put a 10x multiple on that and say it’s worth $2 billion.

Technically we’d need to deduct the brokerage’s equity out of the consolidated BHE equity to adjust the utility’s book value and valuation downwards. I don’t know the real estate arm’s equity but I’d guess it’s fairly small since it’s not capital intensive and it’s certainly not material to the entire company.

Burlington Northern Santa Fe

For BNSF, or any other capital intensive business, I first look at return on tangible capital to try to find an estimate for earnings power for the company as a function of the capital in the business. Many such businesses actually have fairly stable returns on capital, so if you know the level of capital you can estimate average earnings. Here are the numbers for tangible capital employed (TCE), operating income (OI), and return on invested capital employed (ROITC) for BNSF since 2010:

**Note on tangible capital employed: I use total assets - goodwill and intangibles - current liabilities. Another way to think of it is that it’s net working capital + long-term tangible assets. For BNSF specifically, there was a PP&E step-up on the date of the acquisition by Berkshire. I estimate it at ~$12.7 billion; it also looks like this PP&E step-up is not depreciated (based on annual depreciation as a percentage of net PP&E compared against other railroads). Since this PP&E step-up is an accounting convention and not an economic one, I deduct $12.7 billion from tangible capital employed for each year since the acquisition.

The first thing that jumps out at me from this chart is that ROITC is pretty stable. If I told you that in 2030 BNSF will be deploying $100 billion in tangible capital, you’d feel fairly confident in guessing that it will probably be earning ~$14-16 billion in OI. This fairly steady relationship means that for any given level of TCE we can estimate OI.

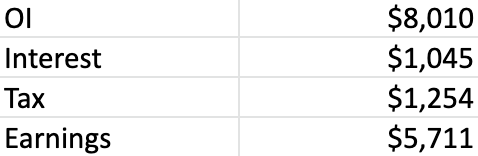

At the end of 2018, BNSF deployed $53.9 billion in TCE. To find its earnings power, I’ll simply multiply this $53.9 billion by its average ROITC of 14.9% since 2010. We have estimated OI of $8 billion.

The next question is how much is that worth? First, it makes sense to map the OI to actual earnings:

I found interest expense by taking BNSF’s current debt load of $23.2 billion and multiplying by the 4.5% blended interest rate that it pays on its debt. I used an 18% tax rate. This is lower than the 21% rate you would expect and what they report on the income statement because railroads benefit from some accelerated depreciation on their PP&E for tax matters. The impact of this can be found under “deferred income taxes” on the cash flow statement for all of the major railroads. As long as the railroads continue to invest capex above their depreciation expense these taxes will be permanently deferred.

Next, I will map those $5.7 billion in earnings to free cash flow so we can appropriately value it. Since we’re assuming a constant ROITC on average, any future earnings growth must be funded by a proportionate amount of growth in the asset base. If BNSF is going to grow its earnings by, say, 4% next year, we would expect that the capital base needs to also increase by that same 4%.

While this exact relationship is unlikely to hold exactly year to year, given the capital intensiveness of the business and the historically stable ROITC, we would expect this relationship to roughly hold over many years. I’m going to assume that BNSF can increase its earnings by 4% annualized through the next economic cycle and that in order to enjoy that growth it will increase its capital base by that same 4% annually.

We can use that general 4% number to find the expected amount of free cash flow conversion. In order to grow earnings at 4% next year it will need to increase its $53.9 billion asset base by that same 4%, or $2.16 billion. However, we don’t need to deduct the whole $2.16 billion from earnings to find free cash flow, because BNSF will finance some of this expansion with debt.

At the end of 2018 BNSF had $23.2 billion in debt outstanding, or 43% of its $53.9 billion asset base. I will assume for this exercise that BNSF keeps the debt to cap ratio at 43%, which means it only needs to fund 57% of the $2.16 billion expansion in the asset base with retained earnings. Therefore, $1.227 billion is funded from retained earnings and $929 million is funded from incremental debt.

We now deduct the equity funded portion of $1.227 billion from the earnings of $5.711 billion earlier to find a FCF number of $4.484 billion. Since we’re discounting this at 10% and assuming 4% growth, we need a FCF yield of 6% to find fair value. That gets us to $74.7 billion of value.

I have tried to be fair but conservative with this estimate. Many investors will correctly point out that Union Pacific, BNSF’s closest peer, currently has a market cap of $120 billion. UP has ~10% more OI, so the thinking goes that BNSF is worth at least $100 billion.

This isn’t a post on railroads, so I’ll keep this part short and sweet. First, I think UP is overvalued, plain and simple. I think the market is underestimating UP’s long-term capital needs and perhaps is also too bullish on long-term volume growth and margins. Second, I had a chance to talk to BNSF’s CFO in Omaha last year, and she said, bluntly, that you shouldn’t assume that BNSF’s profit margins will go up to UP’s levels (like many investors expect) because the route networks and freight mix are different.

All of this said, I think that it is possible that ROITC for BNSF (and other rails) goes up in the future. There is an argument to be made that the past few years have been unusually capex intensive due to positive train control and some other factors. If you think there’s upside to my estimates then you’d mark up the BNSF stake. If you do the same exercise but use a 17% ROITC then BNSF would be worth $90.5 billion. I personally hesitate to assume much better ROITC than 10 years of history have shown us, but I’d love to be proven wrong.

Manufacturing, Service, and Retailing

This segment houses every other operating business that Berkshire owns. This includes Precision Castparts, Lubrizol, Iscar, Marmon, Duracell, and many, many others. For those tracking the segments over time, note that Berkshire combined the businesses in finance and financial products into manufacturing, service, and retailing this year.

These businesses, as a whole, earn excellent returns on invested capital and probably should grow over time at a rate somewhat similar to GDP. I prefer to look at these on the basis of free cash flow yield. I figure they’ll probably grow earnings around 4% or so through the cycle, so I calculate fair value with a 6% fcf yield (adding up to our 10% discount rate).

These businesses as a whole earned $12.3 billion pre-tax in 2018 which would lead to a bit over $9.7 billion after tax assuming a 21% rate. To find free cash flow, we need to deduct capex investment above depreciation and also working capital needs. On page K-107 of the 2018 10-K we can see capital expenditure and depreciation numbers for all of the big business units:

This segment includes manufacturing, McLane, and service and retailing. As a first pass we can see that these businesses invested $1.77 billion over their depreciation expense in 2018. It would be tempting to just deduct that from our net income figure. But if you look at the 2017 numbers you can see that they outspent depreciation by only $928 million, so it makes sense that we we should use a number somewhere in between those two.

It’s difficult to say what a normalized capex number might be without the group balance sheet. While there isn’t much disclosure on what the combined balance sheets look like, we did get the balance sheet for the combined manufacturing, service, and retailing segment in the 2016 shareholder letter:

If you add it all up you have ~$39.6 billion in tangible capital employed (assuming only $2 billion of the cash is actually needed for the operations and taking net working capital + fixed assets + other assets). That number is split about 50 / 50 between net working capital and fixed assets. Since finance and financial products was also added to this segment in 2018, we’d need to add its capital employed as well. There’s unfortunately no way to know that number, but I’ll guess something like $5 billion. In total, then, we had something like $45 billion in tangible capital employed at the end of 2016.

Going back to the capex numbers, we can see that these businesses increased their fixed asset base by maybe 4% ($928 million net capex / $18.9 billion net PP&E in MSR and a bit more for financial products) in 2017 and by maybe 7-8% in 2018 after making the same adjustment for the finance and financial products businesses.

In the two years since we knew part of the numbers, the fixed asset base has grown by somewhere around 10-15%. We guessed there was $45 billion of capital employed then, so let’s guess $50-55 billion now. It seems like a decent guess to say that it’s still roughly half net working capital and half long-term assets.

Going all the way back to our income and growth numbers, we have $9.7 billion in earnings on a capital base of ~$50-55 billion and a decent guess for long-term growth might be 4% or so. Using the same general method as I did with BNSF, we’ll say these businesses would need to increase the capital base by ~4% on average to hit that 4% growth, so a total of roughly $2 billion. Maybe about half of that comes through capex spent over the depreciation allowance and half of that comes through an increase in net working capital. I want to stress that this is a bit of a guess since we don’t have lots of data.

Since these companies do carry some debt, I’ll also say that part of this asset growth is debt financed, so we’ll say that these businesses have free cash flow earnings power of something like $8 billion, assuming they’re growing around 4% over time. Valued at a 6% FCF yield, that gets us to a value of the segment of $133.3 billion.

Some might say that that’s a fairly low number for a segment earning $9.7 billion - it comes out to 13.7x TTM earnings. Feel free to assign a higher number if you wish, but I think more broadly it’s important to factor that this group only has ROITC of ~20-25% - that’s good, not great - and also carries very low levels of debt, which means that you accrue much less free cash flow to the equity than if they had better returns on capital or had a bit more leverage.

Adding It All Up

Going back through the numbers, we have $8.4 billion for the equity method investments, $26.9 billion for the utility, $2 billion for the real estate brokerage, $74.7 billion for BNSF, and $133.3 billion for manufacturing, services, and retailing, which adds up to a total value of $245.4 billion.

Valuation - Insurance Segment

This section will mirror what I did in a previous post on Markel. In that post, I said that for an insurance company you have three main buckets of value - underwriting income, interest income on the fixed income portfolio, and the value of the equities or other productive assets. We will discuss each bucket for Berkshire in turn.

What Does Berkshire’s Fully Levered Balance Sheet Look Like?

This is, in my opinion, one of the most important questions when it comes to valuing Berkshire. The question arises from the nature of an insurer’s balance sheet. Insurers have three sources of balance sheet funding - float, debt, and equity. They generally invest the money from these three sources into a blend of fixed income and equities or other equity-like investments (hedge funds, real estate partnerships, etc.).

A typical insurance company’s simplified balance sheet might look like this:

If you were to value this hypothetical company, leaving aside underwriting profit or loss for now, you would probably count the stocks at fair value then add net interest income. If the fixed income portfolio earned 3% after tax and the LT debt cost 4% after tax, you would have $3.5 of net interest income, so perhaps the total value of the investments would be $20 + $3.5*10 = $55.

The problem with this arises when you shift between fixed income and equity investments. Let’s say now that the company bought a bunch of stocks and now has $100 of fixed income assets and $50 of stocks. If you re-run the numbers, you have $2.6 in investment income, so your fair value is $50 + $2.6*10 = $76.

Did the value of this company increase by 38% overnight as this example implies? Probably not. If this math holds in isolation then why not just invest all of the assets into stocks? Then your value would be $146.

The problem with this kind of analysis is that you’re effectively ignoring the impact of the insurance liabilities. For a well-managed insurance company like Berkshire you won’t have huge capital calls on those insurance liabilities, but you probably don’t want to be investing all of that money into stocks either. No matter how good you are at picking stocks there’s always a risk that you can lose some huge amount of your portfolio. Buffett talks about surviving the 1,000 year storm. If your equity portfolio loses 75% of its value and you’ve funded it with equity, then you survive. If you’ve funded with insurance liabilities, then you probably don’t, one way or another.

To figure out how exactly to value the assets on an insurer’s balance sheet, I like to go back and look at how the company has historically invested its balance sheet and how those investments have been funded. I use this info to see what you could reasonably expect the company to invest in equities (or other productive assets) and what portion will likely stay invested in fixed income, which will be valued on a multiple of the interest income generated.

In my Markel post, I showed a graph of equities as a percentage of the company’s tangible book value. We saw that the company is comfortable investing all of its TBV into equities, so I said that I value the TBV at 100 cents on the dollar and I assumed that all of the rest of the assets (i.e. those funded by debt and insurance liabilities) were invested into fixed income.

Here’s a look back at some of the relevant funding and investment numbers for Berkshire going back to 1998:

Here are the definitions for each column:

Float: total amount of insurance liabilities

Fixed Income: total amount of cash, fixed income investments, and t-bills held in the insurance and other segment

Preferred: total face amount of any preferred stock held by Berkshire

Cash in “Other”: cash held by the operating companies that are held under the “other segment. 2017 and 2018 are estimates because Berkshire stopped reporting this exact number

Fixed Income / Float: (Fixed Income + Preferred - Cash in “Other”) / Float

What are we looking at here? If you look at the Markel post, I had stocks as a percentage of TBV. Their reporting made it relatively easy to find that number. The way Berkshire reports makes it difficult / impossible to find those numbers, so this chart aims to show the exact same metric but just inverted. Instead of looking at stocks as a percentage of TBV we can look at fixed income as a percentage of float. If fixed income is always 100% of float then we know that stocks are 100% of TBV (plus debt, but Berkshire carries low debt so it isn’t that material). If fixed income is less than float, then stocks make up more than 100% of TBV, and vice versa.

What does this chart show? It is basically taking the amount of cash and fixed income securities (I’ll refer to the sum of cash and fixed income just as fixed income from now on) held in Berkshire’s insurance segment and compares that to the amount of float. If fixed income exactly equals float, then the value on the right hand column would come to 100%. If fixed income was below float, implying that Berkshire used some of its float to invest in stocks, then the value on the right hand column would come to less than 100%.

The conclusion is that over the past 20 years Berkshire has generally invested all of its float into cash, bonds, and preferred stock. When people say that Berkshire is using insurance liabilities to invest in stocks, that has generally not been true. They invest insurance liabilities into fixed income instruments and their retained earnings into stocks, more or less.

What does this mean for our valuation? If Berkshire routinely invested most or all of its float into stocks, you could correctly say that you should value the portion of its investments financed by float at 100 cents on the dollar. Since it does not do this, and since that money is generally invested into fixed income securities, the value that an equity holder derives from it consists of the net present value of the interest income from those fixed income securities. That is how I will value it.

Three Buckets of Insurance Value

As I mentioned previously, the three buckets of value creation for any insurance company are underwriting income, interest from fixed maturity securities, and excess cash and productive investments. I will value each in turn.

Underwriting Income

I break out the underwriting businesses into Geico and Other. I do this because Geico’s performance has been so strong that grouping it with the other segments would undercount its value.

Geico has been probably one of the best performing companies in the world over the last couple of decades. If it was public its stock would have been a home run. Premiums earned are up from $10.1 billion in 2005 to $34.1 billion in 2018, for a CAGR of 9.8%. Over that time Geico has underwritten at a profit in all but one year and has averaged a combined ratio (1 - operating profit margin) of 94.1%.

I value Geico by taking TTM premiums of $34.1 billion, multiplying them by a 5% profit margin (being a bit conservative relative to the 94.1% CR historically), subtracting a 21% tax rate, and giving that income stream a 25x multiple. That gets a value of $33.7 billion.

Some might think that a 25x multiple is way too high, but with a long history of 10% organic premium growth and high and consistent profitability through the period, it’s clear that the underwriting income stream is worth a lot.

For the other segment, which consists of a bevy of insurance and reinsurance operations, I value things on more of an average basis over a few years. These operations can and do have lumpy results, so it doesn’t make sense to use a single year’s results. Premiums written over the last five years averaged $22.8 billion. That average grew at roughly a 1% CAGR over the 5 year average before that, so we shouldn’t expect too much growth from this segment.

Over the last 15 years this segment has underwritten at a combined ratio of 95.4%. To value it, I multiply the average of 5 years’ premiums of $22.8 billion by a 4% profit margin, 21% tax rate, and attach an 11x multiple, which comes out to a value of $7.2 billion. I use the 11x multiple because in assuming 1% organic growth in premiums (found earlier) we’d need a ~9% FCF yield to discount to our 10% rate.

Our value for each piece of underwriting income adds up to $40.9 billion.

Investment Income from Fixed Maturity Investments

This is where we’ll use the info about the fully levered balance sheet. At the end of 2018 Berkshire had $123 billion of float. If we go by what I said earlier, we would assume that with a fully levered balance sheet Berkshire would still have $123 billion in fixed maturities, so we would take $123 billion and multiply by the interest rate we’d expect Berkshire to earn on those investments over time.

I’m going to walk back what I wrote earlier a bit. A bit! It looks to me that while historically Berkshire hasn’t invested the insurance liabilities into productive assets, Buffett might be more willing to do that now. Berkshire has gotten so huge and there’s so much extra capital that I think there’s a bit less risk into deploying some of the float into stocks or businesses. Because of that, I now assume that Berkshire will keep fixed income equal to at least 80% of the float. Everything else I count as excess cash and value at 100 cents on the dollar.

Applying that to our current numbers, we have 80% of $123 billion that I think Buffett will keep in fixed maturity securities. Since Buffett is so conservative, on maturity length and credit quality, I use 2.5% after tax for an expected interest rate for these investments. That gets us to $2.5 billion of annual after-tax interest income. I put a 7% fcf yield on that to find fair value, as blending Geico and Other’s growth rates would get you to about 3% annual float growth. That gets us a value of $34.4 billion for investment income from the fixed maturity securities.

Excess Cash

The last bucket is in the investments that are truly excess to the insurance requirements and can be deployed into productive assets. Since I used 80% fixed income as a percentage of float, it stands that any other financial assets should be counted at full value.

Here’s the 2018 consolidated balance sheet to help you see what I’m doing here:

The only adjustment I make is for cash needed for working capital at the different operating subsidiaries. I assume that all the operations need ~$5 billion in cash just to run, so I take total cash and then deduct $5 billion for working capital needs.

If you add up “cash and cash equivalents,” “short-term investments in U.S. treasury bills,” “investments in fixed maturity securities,” and “cash and cash equivalents” from the Railroad, Utilities, and Energy Segment, you get $131.7 billion. Deduct $5 billion for working capital and you get $126.7 billion. Since we said that we need 80% of the float to stay in fixed maturities, that means that the difference between $126.7 billion and 80% * $123 billion is truly excess. That totals out to $28.3 billion of excess cash that I’ll value at 100 cents on the dollar.

Equity Securities

The last step is to value the equity securities. I do this by tracking the number of shares of the biggest holdings (Apple, Bank of America, Wells Fargo, Coca-Cola, American Express, and Kraft Heinz) and then assuming the rest of the portfolio does as well as the S&P 500.

As I write this, pulling the shares owned by Berkshire on 12/31 forward to today and using today’s prices, Berkshire’s stock portfolio should be worth ~$201 billion. This is up from $187 billion (Kraft Heinz is included in this bucket even though its held under equity method investments on the balance sheet) at the end of 2018.

I prefer to make a few adjustments to this number (or have you guessed that by this point?).

First, I pretty much assume that Berkshire will be holding its stock investments indefinitely, so the present value of these comes completely from the dividends. Since Berkshire pays some tax on those dividends, I think it makes sense to deduct the value of those taxes. Buffett mentioned in the 2018 letter that Berkshire pays ~13% tax on dividends from its stocks in the insurance segment (Separate note: this seems much too high to me just based on the fact that they should get a 70% deduction and their tax rate is 21%. Does anyone know the reason why they would pay 13% instead of ~6%?), so I reduce the value of these stocks by that same 13%. Kraft Heinz is held outside of insurance, and Berkshire only owes ~4.2% tax on these dividends (80% deduction on a 21% tax rate) so you should only take 4.2% off of that value. After deducting 13% from the value of the stocks in the insurance segment and 4.2% from Kraft Heinz, you get a value for the equity portfolio of $176 billion.

Second, I don’t love to blindly mark each equity holding at its market value. If some holdings look expensive then you’re effectively saying they’re worth that expensive price. I take all of the big positions except for AmEx (Apple, Bank of America, Wells Fargo, Coke, and Kraft Heinz) and mark them to the lower of market value or a price where I conservatively think I’d need to buy it to make 10% over time. I exclude AmEx because I don’t have much to say about that and the stock looks cheap enough. For the rest of the stocks, I value them by proxy as the S&P 500 like I mentioned earlier.

You can come up with your own values for the stocks, but I value Apple at 10x trailing earnings ex cash ($142.51), BAC and WFC at 1.8x TBVPS ($32.24 and $57.35, respectively), Coke at 20x my estimate of owner’s earnings ($37.50), and Kraft Heinz at roughly an 8% free cash flow yield ($36.85). I’m trying to use conservative values here, as you can probably tell. Marking the values down might seem a bit silly, but it helps in situations like when KHC is trading at $90 and it’s pretty clearly worth no more than $50. If you mark it to something conservative, your valuation of Berkshire isn’t beholden to a sometimes frothy market.

I value the S&P 500 at 2.5x book value, which on $843.58 of book value comes out to 2,109. I could write a whole article on this but suffice it to say that I’m using a 10% discount rate and stocks probably don’t make 10% from here over time from current levels.

Using the lower of estimated value (for Apple, Coke, and the market) and market value (for Kraft Heinz, Wells Fargo, and Bank of America) I get total value of $175 billion. After multiplying each number by its tax rate, as I did in the previous section, I get a total value of $153 billion.

Adding It All Up

Going back through the numbers, we have $40.9 billion for the underwriting income, $34.4 billion for the investment income, $28.3 billion in excess cash, and $153 billion for the equity portfolio, which adds up to a total value of $256.6 billion.

Consolidated Valuation

Now we just need to add everything up. We had a value of $245.4 billion for the operating companies and $256.6 billion on the insurance side.

The last piece is that Berkshire does have some liabilities at the parent level. It has $16.9 billion of debt, which incurs $367 million of annual interest expense. It also has a notional liability of $2.5 billion on its derivative bets (although that number is likely lower marked to market as of today compared to the relative lows at the end of 2018). If we capitalize the interest expense we get a value of $2.9 billion and after adding the derivative liabilities we get a total value of -$5.4 billion.

To sum up, we have $245.4 billion + $256.6 billion - $5.4 billion for a total value of $496.6 billion. There are 2.46 billion class b shares outstanding, so that translates to a total value per share of $202.

Conclusion

I have tried to go through each business and value it based on the underlying cash flows that it is likely to produce. I tried to use conservative, although not overly harsh estimates and think through situations where conventional valuation wisdom might overlook important variables.

The biggest valuation gaps between what I’ve done and what others tend to do generally exist for two reasons. First, I do not believe that most of the investments on Berkshire’s balance sheet should be carried at 100 cents on the dollar. Second, the operating businesses that Berkshire owns are good on aggregate, they are not exactly great. If you’re assuming growth, which I think is a fair assumption, you need to account for the working capital and capex needed to fund that growth.

Stepping back a bit, you have a large conglomerate with a diverse stream of cash flows and lots of net cash on the balance sheet that looks conservatively priced to make 10% or so annually. That looks pretty attractive given the risk profile.

That is quite enough for now. I'll have a follow-up at some point that looks at actual intrinsic value growth over time, some thoughts on future capital allocation, and using Berkshire as your opportunity cost.

Disclosure: Pursuant to the provisions of Rule 206(4)-1 of the Investment Advisors Act of 1940, we advise all readers to recognize that they should not assume that recommendations made in the future will be profitable or will equal the performance of past recommendations. This publication is not a solicitation to buy or offer to sell any of the securities listed or reviewed herein. This contents of this publication are not recommendations to buy or sell any of the securities listed or reviewed herein. Investing involves risk, including risk of loss. The contents of this publication have been compiled from original and published sources believed to be reliable, but are not guaranteed as to accuracy or completeness. Kyler Hasson is an investment advisor and portfolio manager at Delta Investment Management, a registered investment advisor. The views expressed in this publication are those of Kyler Hasson and not of Delta Investment Management. Kyler Hasson and/or clients of Delta Investment Management and individuals associated with Delta Investment Management may have positions in and may from time to time make purchases or sales of securities mentioned herein.

[jetpack_subscription_form show_only_email_and_button="true" custom_background_button_color="undefined" custom_text_button_color="undefined" submit_button_text="Subscribe" submit_button_classes="undefined" show_subscribers_total="false" ]