Some Thoughts on Markel After a Tough Year

Disclosure: I own a tiny bit of Markel (literally 1 share) for a client. More broadly, I generally like the company and wanted to go over some of its strengths and weaknesses and a rough estimate of its valuation.

Markel has been one of the better managed insurance companies over the past couple of decades. Its playbook has been something like Berkshire Hathaway’s - consistent underwriting gains, a fairly low-risk fixed income portfolio, a large equity portfolio relative to other insurers, and in the past 10 years or so a growing commitment to buying businesses outright. While the playbooks are similar, Markel is less than 5% of Berkshire’s size, as measured simply by total assets. This smaller base, coupled with a larger concentration of value in its insurance business, should hypothetically mean that Markel can compound its intrinsic value at a higher rate than Berkshire. Indeed, over the last 20 years, book value per share at Markel is up 775% while Berkshire’s is up 503%.

Although growth has been better than Berkshire’s over a long time frame, Markel’s performance over the last few years has been something less than strong. The company has invested significant sums of money into Markel Ventures, its buyout arm, and a couple of reinsurance asset managers held in its other segment. While these new portfolio companies have added to Markel’s earnings stream, Markel has had a few writedowns in this segment, culminating with a total goodwill impairment in its Catco business and a large loss in funds directly invested in Catco’s products. Many investors feel that the company would do better to stick with investing in public securities, a strategy that has worked well in the past, as the longer-term track record indicates.

A poor year this year has sent the stock down from a high of ~$1,200 to about $1,000 and in general has taken some of the premium off of shares, so I think it’s a good time to examine its valuation. I’m going to value its insurance and non-insurance segments separately then add them up to find the value of the total company.

Valuing Insurance Companies

There are the three buckets of value for any insurance company - underwriting gains or losses, investment income from fixed income, and gains in its equity portfolio. I’ll make a few assumptions so that I can assign a value to each bucket. In general, insurance tends to be very lumpy from year to year, both on the underwriting and investing sides, so I try to think about returns over much longer periods to smooth out the results.

Underwriting Gain / Loss

My preferred method to find the value of any underwriting operations is to take TTM premiums earned and multiply by an average combined ratio. Markel’s combined ratio has been ~96% over 5, 10, and 15 years, so I’ll use that number. TTM earned premiums were $4,711mm, so we’d expect average, pre-tax underwriting income of ~$190mm, or $150mm after tax.

Fixed Income

Based on a rough number from its earnings release (the annual report hasn’t been released yet), Markel has $13,440mm of fixed income investments. I assume 3% after tax yields on its fixed income portfolio, which is a bit above the returns it has made over the last 5 years or so, but I would generally expect higher average interest rates over time. Markel does keep its fixed income portfolio very safe - over 90% AAA / AA, so don’t expect a huge yield spread over treasurys.

To make things simpler, I net out interest income with interest expense so that I can throw it all into one bucket. Markel currently has $3,010mm in consolidated debt at a ~5% interest rate. Since we’re assuming slightly higher average rates for the bond portfolio, I’ll also assume slightly higher average rates on the debt. I’ll call it 6%, for net interest expense of $180mm, or $143mm of expense after tax (apples to apples since I’m also using after tax numbers on the income from the bond portfolio).

Netting the two numbers out, we get interest income of $260mm.

Equity Portfolio

Markel had ~$5,760mm in stocks at the end of 2018. If I was marking them to market as of today, the S&P is up ~10% YTD, so call it $6,336mm in stocks. For Markel, I tend to just value the stocks at 100 cents on the dollar. If you had a view that stocks were severely under or overvalued, you could adjust the “fair value” of Markel’s stocks up or down.

Total Valuation

I use a sum of the parts valuation, which just add up all of the buckets. We have $150mm in underwriting income, $260mm in net interest income (net as in after-tax and net of all interest expense), and $6,336 of value in equities. A conservative value might be 10x underwriting income + 10x interest income + total equity value, which would come out to ~$10.4 billion.

I’m using 10x underwriting and interest income to try to be a bit conservative. If the company doesn’t grow premium volumes at all, then you’d expect roughly no growth over time in either of these buckets, so I’m effectively underwriting this to a 10% IRR at no growth. As we’ll see in the next section, growth can really supercharge intrinsic value growth.

Thoughts and Considerations

I think that’s a fairly conservative value of all the insurance buckets. Here are some general puts and takes:

Risks:

Climate change could lead to higher combined ratios over time. Buffett has said that climate change would actually be good for insurance companies as more risk would lead to higher industry wide dollar premiums. I agree with his logic, but he’s effectively assuming a constant combined ratio. If it takes some time for models and pricing to adjust, or if climate keeps proving a bit worse than expected, then that could push up combined ratios in the future.

Reinsurance kind of sucks. It hasn’t been a great business in the past few years, and it doesn’t look like pricing is improving any time soon. Reinsurers have faced competition from institutional investors, who have lower costs of capital (for now), which has depressed pricing. If cheap capital stays in reinsurance, it could severely impact combined ratios and returns for reinsurers, including Markel.

Interest rates might stay low. I am using an average interest rate above what prevails today, so continued lowish rates could hurt returns on the fixed income portfolio. That would be partly mitigated by lower rates on Markel’s own debt.

Stocks might be expensive. No real comment here, but with such a high percentage of the company’s value in stocks, a weaker stock market (or bad stock picking) could mean that I’m overvaluing the company as a whole.

Opportunities:

Positive exposure to rising interest rates. If rates really increase, Markel’s fixed income portfolio will become much more valuable. It’s sometimes difficult as an investor to get positive exposure to rising rates. It’s also nice that insurance tends to be non-cyclical as opposed to banks.

Tom Gayner is usually pretty good at picking stocks! He’s beaten the market by a couple of percentage points annually over time, so with this sort of valuation you aren’t really taking good stock picking into account.

Compounding In Insurance

As a fairly long-term holder and also fan of Berkshire (disclosure: long for myself and clients), compounding of intrinsic value in insurance is near and dear to my heart. I think that the value drivers are relatively misunderstood but also incredibly important.

We talked about earnings in the last section, but I want to switch to looking at book value for a minute. In modelling out intrinsic value growth, I like to look at tangible book value in the insurance segment, because that drives what’s really going on behind the hood. Let’s take a look at some numbers.

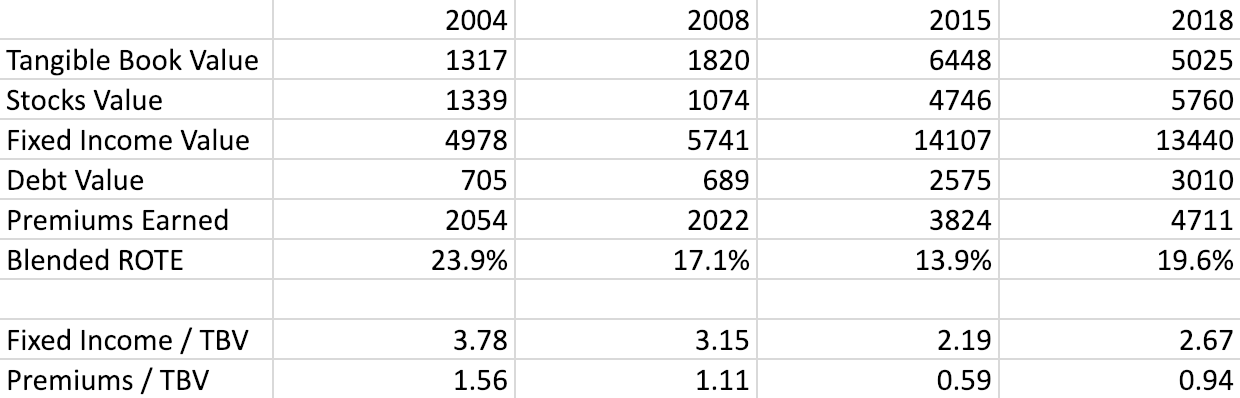

Here is a chart showing some key numbers and ratios for 2004, 2008, 2015, and 2018:

I’ll call your attention to the “Blended ROTE” number. This number takes the estimated annual income, just like we calculated it in the previous section, and uses that to compute a ROTE. Tangible book value is what is allocated to the insurance segment. Since the start of Markel Ventures after 2008, I’ve used an estimate based on the ventures equity and goodwill entries from the 10-Ks. As an estimate, the true numbers are going to be a bit off.

If you go back to 2004, you would see that in a year where Markel made a normal underwriting and fixed income investing profit and also made 10% on its equity portfolio, tangible book value would increase by 23.9%. That’s pretty good! But if you look at a chart of Markel’s stock price, it has not exactly compounded at 23.9% since then. What gives?

The insurance model is quite beautiful. If you can underwrite profitably, and if you roughly allocate all of your TBV to equities (as Markel did, roughly, in 2004), then you can earn your normal equity return plus the contribution from your fixed income portfolio, which is largely financed by insurance float, and insurance underwriting. The extra income can be quite substantial, as these numbers show.

The challenge, however, is to not have excess capital pile up. If you had Markel’s numbers in 2004, made those average returns for four years, and didn’t increase your underwriting premiums, then your economics look a lot different. After those four years, your TBV has doubled (close enough), but your run-rate ROTE would be much lower: if you still had your whole TBV in equities, ROTE with the same inputs would be 17%. That’s still excellent, but obviously decreasing.

In 2004 you basically had $180mm in income from underwriting + fixed income, then you got a (hypothetical) 10% return on your $1.3bb equity portfolio. If you didn’t increase underwriting for four years then you’d still have that $180mm run rate other income but on a $2.6bb equity portfolio (assuming all net income went into equities). You’re still making good money, but the boost you get on your equity portfolio is much smaller.

The key that really leads to compounding is organic premium volume growth. If you started with the same numbers but grew premiums along with TBV, then you’d actually compound at that 23.9%. After four years you’d have a $3.1bb equity portfolio with $424mm in other income. The difference is that the higher premiums give you proportionately higher run-rate underwriting income along with more fixed income earnings from higher float. You want to keep up your fixed income / TBV and premium / TBV as high as you can so that you can keep getting that boost to your equity returns.

Obviously, it’s pretty much impossible to double premiums over four years while still writing good, profitable business. The problem that pretty much every well-run insurance company has is that it generates tons of capital and loses the embedded leverage inherent in the model. Incidentally, strong premium growth is what really supercharged Berkshire’s returns up until 2000. I think Buffett should get much more credit for this, but that’s a post for another day.

If you look back at the chart, you can see that Markel has largely struggled with re-levering its growth in assets to its insurance business. The company has acquired different insurers to get higher premium volumes and float and also started to allocate money in other segments, but the company has generated lots of excess capital. As you can see, the ratios of fixed income / TBV and premiums /TBV have declined fairly significantly since 2004. If Markel hadn’t allocated money to acquisitions, the ratios would be much, much lower. So you really don’t get that super high rate of compounding that you’d get if you could increase your premiums along with TBV, but the returns can still be strong if you allocate capital well.

This phenomenon is why I don’t like to value Markel on a P/B basis. It makes more sense to figure out the run-rates for underwriting and fixed income earnings and simply add that to the equity portfolio. If you say that it’s worth 2x TBV and they don’t increase premiums at all for 5 years and keep all of the capital in the insurance business, then TBV will roughly double. The value will be higher, but the deserved premium to TBV will be lower as they would benefit from underwriting + fixed income earnings at proportionately half the rate.

With all of this in mind, I want to go back to the 10x multiple for the underwriting + fixed income earnings. I underwrite Markel at a 12% IRR (more of an opportunity cost thing than a real fair value consideration). My underlying assumptions are for ~2% organic premium growth, which would get me to a 12% IRR with a 10% earnings / fcf yield.

Valuing Markel Ventures and Other

This is a little more straight forward. My method is to take EBITDA - capex, convert that to fcf, and underwrite it at a 12% discount rate. EBITDA - capex was $166mm for 2018, excluding a $48mm writedown. Call that roughly $130mm of earnings after tax and maybe $125mm of fcf after taking working capital into account if the earnings are growing. I assume these are relatively low growing businesses (say 3%), so I’ll value them at a 9% fcf yield or $1.4bb.

If you recall, I allocated all of the consolidated debt to the insurance segment, so I’m ignoring any interest costs here. I’m also ignoring any amortization shields on taxes, but the numbers are probably close enough. If you want to look at it on an EV / EBITDA basis it comes out to 6.4x, which is a bit higher than likely multiples for these individual businesses but in my opinion makes sense for a broader collection of smaller businesses (less individual company risk because of diversification and cheaper access to financing as a part of Markel, so the multiple should be a bit higher).

The last parts of the valuation are Markel CatCo, State National program services, and Nephila.

I’m going to assume $0 value for Markel CatCo’s earnings after the recent problems there.

State National program services, which is the portion of that company which isn’t reported in the insurance segment, earned $71mm last year, as best as I can tell. I’ll put a 10x multiple on that, again assuming low growth and a 12% discount rate, for a value of $711mm. That seems roughly correct as Markel bought the business for $919mm at the end of 2017 and part of the value lies in the insurance segment.

The last part of the value is Nephila. Markel bought Nephila for $975mm late last year, so I’ll just keep that as a placeholder until we see the results from that business.

Adding up all of these parts, we get a value of $3.1bb.

Markel’s SOTP

Adding up the value from the insurance segment of $10.4bb plus the $3.1bb from ventures and other, we get a total value of $13.5bb. With 13,888mm shares outstanding, that gets to a value of ~$972 / share using a 12% discount rate, ~2% earned premium growth, and LSD earnings growth over time at ventures and other. You can go back and re-underwrite everything to 10% (or whatever other number you’d like) as you have all of the relevant numbers.

There is definitely some wiggle room on that, as arguably fair value would have a lower discount rate. Again, for me, it’s more of an opportunity cost issue. On the flip side, I did value the equities at 100 cents on the dollar, and they won’t be making 12% IRRs on their equities from these levels over time.

There are two big questions in my mind when it comes to the valuation.

First is the rate of organic premium growth. If somehow Markel could grow premiums at 5% or so while still keeping underwriting discipline, then the intrinsic value creation on the insurance side would be quite substantial. They would be increasing their run-rate for underwriting income and increasing float, which would lead to higher earnings on its fixed income portfolio, and all of that would combine with the equity portfolio to compound that growth at a great rate over time. If you look back at Berkshire’s premium growth over time, they would go through long periods of low to no growth during tough insurance markets then would ramp to huge growth rates when pricing was suitable. If something like this happened at Markel, the value of the insurance business could easily double in a few years, and this valuation does not take that possibility into account.

The second big question on valuation is capital allocation. It seems weird to say since they have historically been great capital allocators, and I really like Gayner. I have great confidence in their public equity portfolio, but there have been a lot of writedowns in the ventures and other segment. Furthermore, Gayner has deployed a lot of capital into ventures and other over the past few years, so if the results turn out poorly then Markel will suffer as a whole. I’ll examine the track record in a separate (shorter!) post.

Disclosure: Pursuant to the provisions of Rule 206(4)-1 of the Investment Advisors Act of 1940, we advise all readers to recognize that they should not assume that recommendations made in the future will be profitable or will equal the performance of past recommendations. This publication is not a solicitation to buy or offer to sell any of the securities listed or reviewed herein. This contents of this publication are not recommendations to buy or sell any of the securities listed or reviewed herein. Investing involves risk, including risk of loss. The contents of this publication have been compiled from original and published sources believed to be reliable, but are not guaranteed as to accuracy or completeness. Kyler Hasson is an investment advisor and portfolio manager at Delta Investment Management, a registered investment advisor. The views expressed in this publication are those of Kyler Hasson and not of Delta Investment Management. Kyler Hasson and/or clients of Delta Investment Management and individuals associated with Delta Investment Management may have positions in and may from time to time make purchases or sales of securities mentioned herein.

[jetpack_subscription_form show_only_email_and_button="true" custom_background_button_color="undefined" custom_text_button_color="undefined" submit_button_text="Subscribe" submit_button_classes="undefined" show_subscribers_total="false" ]