Altice

My Last Levered Value Investment, I Swear

Cable Overview

This is not meant to be a cable write-up. Plenty of people have written about the industry, and if you would like to get up to speed on cable, Andrew Walker at Yet Another Value Blog has done some great posts on Charter, and @find_me_value has a couple of terrific decks (paywall) if you’re trying to get to know the space.

I do want to quickly answer one question, which is why has cable historically worked so well?

Over the past 5-10 years, the story has been pretty consistent. Since content costs eat up most of the profitability of the video business, most of cable’s economics are driven by broadband subscribers. And the broadband story has been very strong - broadband penetration has increased mostly at the expense of lower speed DSL offerings, pricing has gone up, margins have gone up, capex as a percentage of revenue has gone down, and most cable companies have used the cash flows generated from their assets to buy back shares, so share counts have gone down.

In short, every relevant variable is moving in the right direction. None of these metrics are up tremendously by themselves over the past few years, but the combination of everything working together has led to 20%+ annualized FCF / share growth for most cable companies.

Moving forward, the main risks facing cable companies in general are more fiber overbuilds of their footprint, potential threats from 5g wireless internet service, lower DSL market share (so less market share easily available to take), and potential limits on ARPU growth, either from a combination of the above or via regulation.

Altice Asset Overview

Altice owns two distinct cable assets - Optimum and Suddenlink. Optimum operates in the tri-state area, excluding Manhattan, while Suddenlink has a more scattered footprint that covers parts of West Virginia, North Carolina, Texas, Oklahoma, California, Arizona, and some other states.

I estimate that Optimum has ~5.2mm passings, while Suddenlink has ~3.8mm, which gives Altice a total of around 9mm.

Optimum faces intense fiber competition from Verizon FIOS, with roughly 60% of its passings overbuilt, compared to ~30% fiber penetration of Charter and Comcast’s footprints. Suddenlink, on the other hand, has relatively low fiber competition, but its cable plant is not always the highest quality, with low offered speeds across roughly 20% of its network.

In general, Altice is known for high broadband pricing along with poor customer service. Its penetration across its Suddenlink footprint is particularly low given a small amount of fiber competition: customer penetration is estimated around 45%, which compares unfavorably to penetration across Charter or Comcast’s footprint of close to 60%. Management has generally chosen to squeeze its assets hard for current cash flow with their high price / low cost model. This is in stark contrast to Charter, specifically, which follows the opposite approach - it has relatively low pricing and has invested to insource high-quality customer service support, which has led to relatively much lower profitability per passing but much higher customer growth. In my opinion, there is no obvious answer to which is the better strategy, but Charter’s strategy certainly means that it has more growth in its future.

The last relevant piece for understanding Altice’s footprint is that the company is currently undergoing three relatively large capital investments.

First, Altice is replacing most of its Optimum footprint with high quality fiber of its own. This will increase the speed and quality of the network, which will help it compete more effectively against Verizon’s FIOS offering. Out of its 5.2mm total passings, it will overbuild all of the ~3mm passings that compete directly with FIOS, along with ~500k additional passings.

Second, Altice is building edge-outs across its Suddenlink footprint which will add ~150-200k new passings per year for the next 5 or so years. Many of these passings are to newly built communities in Texas and Oklahoma. Some more are into areas that are underserved and they think they can take share. Management thinks that they can get ~50-60% penetration in these areas.

Third, Altice is upgrading ~400k out of its ~700k households in the Suddenlink footprint that currently have low speeds. Current penetration in these households is in the range of 20-30% and management thinks they can get penetration close to 50% with the upgrades.

Why do investors dislike Altice?

Altice trades at a large discount on current earnings metrics compared to Charter and Comcast, and many Charter and Comcast investors are just not interested at all in the company. Here are the relevant concerns that people have:

Preference To Own Charter

First, many people ignore Altice because Charter and Liberty Broadband (a discounted holding company for Charter) exist. Charter is a great company and it has a lot of things going for it. As mentioned above, it has a relatively customer friendly, high-growth playbook. It is also quite profitable as it exists; it has a long runway for pricing and margin increases; it currently faces a relatively low amount of fiber competition; it has a simple capital allocation framework of buybacks with a reasonable leverage target; and it is executing tremendously in its newer mobile offering, which should be immensely profitable in its own right and should also reduce customer churn over time.

This is not a Charter write-up, but I will simply note that most investors think that Charter can make something like 10-13% annualized returns over time, and if you hold it through Liberty Broadband, your IRR is likely to be perhaps 2-3% higher.

If you like the cable business, then you probably like Charter given its obvious quality. If you are going to own ATUS, given that it is a lower quality company, your opportunity cost should start with what you think you’ll make in Charter / Liberty Broadband. We’ll call the opportunity cost 15% annualized returns.

Optimum and Suddenlink Are Vulnerable

It will be difficult for Optimum to grow subscribers given Verizon’s high overlap with its fiber FIOS product. Additionally, it will be difficult for both Optimum and Suddenlink to grow given already high pricing throughout their footprint, especially paired with the fact that Altice has cut costs and so its customer service is generally quite poor. That strategy has meant high current profitability, but it makes it more difficult for the company to compete against new entrants, and could lead to outright subscriber losses.

Patrick Drahi - Majority Owner and Known Rascal

Patrick Drahi owns roughly 50% of Altice, and with share repurchases his ownership in the company will increase at a high rate. He is known to show little regard for minority shareholders, executing takeovers of telecom assets in Europe at low valuations.

Altice is likely to repurchase 10-15% of its shares outstanding per year over time, so in that scenario Drahi would own a large majority of the shares relatively quickly. It is fairly likely that at some point he will attempt to purchase the rest of the company from minority shareholders. If he times this effort when the stock is undervalued, investors could be forced to sell their stock for less than what they believe it’s worth.

Rumored Mint Mobile Deal

This is just a rumor, but the New York Post ran a story that Altice was in discussions to buy Mint Mobile, a wireless MVNO provider. While this would have some benefits where Mint Mobile overlaps with Altice’s footprint, it doesn’t make any strategic sense over then areas that Mint Mobile’s customers don’t overlap with Altice’s cable customers. This is just a rumor, but it doesn’t make much business sense, and if they do buy it there’s little doubt in my mind Altice’s stock will be down 10%+.

Why I Own It

All of the above worries are very real and very fair, and yet I still own Altice. I believe that investors are right to price Altice at a significant discount to Charter on current profitability, but in my opinion, the discount is currently too wide. The root of this is that I think both Optimum and Suddenlink are actually better than investors perceive.

Recent Results

What we’re worried about is how the results look going forward, but it should be noted that broadband penetration has been slightly up each of the past three years (with a larger increase in 2020 due to COVID). So even with all of these asset quality and pricing issues, Altice is still increasing penetration across its footprint.

Like other cable companies, they have paired higher broadband subscribers with mix shift to higher broadband speeds, higher absolute pricing, and higher margins.

Competitive Environment

For Optimum, they have already faced high levels of fiber competition over most of their footprint for 10 years. That makes the penetration and profitability of the system lower than it otherwise would be, but importantly, this is not new competition. It isn’t an increase in the competitive intensity. And when you take Optimum’s upgrade of their own network into account, you realize that their competitive position is actually getting better. The fiber will increase speeds, increase reliability, increase customer satisfaction, and decrease churn.

Altice likely earns 60-65% of its total income from its Optimum footprint, and results there should improve. Unless results at Optimum are significantly worse than the combined results with Suddenlink, we know Optimum is already keeping steady penetration or growing slightly, so we should have some growth in the future.

For Suddenlink, the outlook is somewhat more uncertain. They don’t run the Charter playbook that I like (low pricing, good customer service, high growth), and while they currently face low amounts of fiber competition, more fiber will be built across their footprint in the future. The competitive environment will, indeed, get more difficult.

However, that being said, there are a couple of very real positives for Suddenlink. They have a little over 700,000 passings where they provide low speeds and have low penetration (~20-30% per management). They will be able to upgrade ~400k of these passings, which could take penetration up to Suddenlink’s average of close to 50%. That could lead to roughly 100k incremental subscribers.

They are also performing a large amount of edge-outs (building plant into new or previously underserved communities). Between normal edge-outs and incremental opportunities around their recent acquisition of Morris Broadband, they should be able to build ~150-200k new passings per year over the next five years. At normal edge-out penetration of ~60%, that’s another incremental ~100k broadband subs per year.

When you add these two projects together, you might have ~120k new broadband subs per year on a base of roughly 1.7mm subs for Suddenlink’s whole footprint. That is ~7% subscriber growth. Even if their penetration on the current base is slightly down due to increased competition, Suddenlink should still be able to grow subscribers.

Will Drahi Steal This?

I do believe there is some risk here, but I think we need to try to be specific about what might happen.

Drahi has taken over assets at perceived discounts to their true values in Europe. However, rights for minority shareholders are stronger in the US. In my opinion, there is risk that Drahi squeezes out minority shareholders in a few years when he owns much more of the company at a price that investors aren’t thrilled with, but I think he has to offer a somewhat fair valuation.

Given the cash flow metrics, it is hard for me to see Drahi being able to buy this out from shareholders at, say, 8x EBITDA. At 8x, the math is very clear that with decent cable results equity returns will be incredibly high.

It seems more likely that a downside case on his eventual purchase multiple is around 9x. At 9x this would probably still be too cheap but perhaps it’s arguable that that’s a reasonable valuation. Please note, that 9x would still be at a large discount to where peers have transacted. Here’s some good work by (again) Andrew Walker detailing some recent comparable sales prices in the space. To be clear, they are all much higher than 9x. But we’re trying to be conservative.

If you are buying into Altice at a multiple of 11x, and with 5.5x turns of leverage on the company, if you get bought out at 9x a few years down the line, you’re going to be in a world of hurt. But if you buy it at 8.5x, which is roughly where it trades now, then if you get bought out at 9x then that sucks, but as long as intrinsic value has grown in the meantime, you’ll probably end up going okay.

Practically, I just make sure to underwrite Altice at a constant (and low) multiple to make sure that I’m not assuming some fantastic result where the valuation really expands. I try to do this in order to be conservative anyways, but in a world where Drahi could take this over at a relatively cheap valuation, I think this is extra prudent.

As I move into a discussion to the current valuation and what we need to see in order to make a return above our opportunity cost, it is important to keep all of the following in mind:

Broadband penetration has been slightly up over the past few years

Optimum’s competitive position is improving

Suddenlink will face more fiber competition, but from new builds and upgrades should be able to add 100k+ broadband subscribers annually off of a base of ~1.7mm.

We need to be hesitant to assume much valuation expansion given Drahi’s presence

Valuation (Written on 8/26/21 with the stock just under $28)

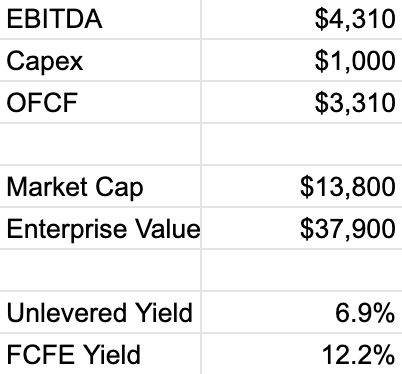

Investors have generally valued cable businesses on EV / EBITDA (and I’ve used it above for shorthand and ease of comparison), but given changing capex needs over time, in my opinion it is better to use multiples of operating free cash flow (OFCF), which is definted as EBITDA - capex.

Three quick housekeeping items:

I take out $100mm from EBITDA numbers, $60mm of capex, and $700mm of debt to account for a non-controlling interest resulting from Altice’s partial sale of Lightpath, their enterprise business. I also deduct an additional $100mm to account for share-based compensation.

I add $50mm to EBITDA numbers for current mobile losses. While their mobile offering is not as strong as Comcast or Charter’s, it is very likely that this spend is NPV positive.

I find it easier to look at valuations by capitalizing the FTTH spend. I assume that Altice spends $1B in total between 2021-2023. I deduct this spend from capex estimates and add that $1B to the market cap and enterprise value of the company.

With those two adjustments, we have the following valuation metrics:

As you can see, Altice carries significant leverage, with net debt / EBITDA at 5.6x. If you are skittish on leverage, then this is not the company for you, but this is hardly extreme for a cable company. Charter, for example, carries ~4.5x leverage.

Reverse DCF - What do we need to hit high-teens IRRs?

Given the above financial metrics, what level of EBITDA growth do we need to hit high-teens IRRs? If we can make high-teens, that should compensate us with a higher return than what we can expect from holding CHTR / LBRDK.

If we assume a constant EBITDA multiple of 8.5x and that all of the free cash flow goes towards repurchasing shares, then 2% EBITDA growth would give IRRs of close to 19%.

You can run any kind of sensitivity that you’d like (the company pays down more debt, the valuation multiple changes, they refinance some debt and save on interest costs, etc. etc.) but to me the most important one is the pace of EBITDA growth.

If EBITDA dollars are flat (please note that I have a $40mm bump in 2022 EBITDA due to accretion from its recently completed Morris Broadband deal), then your IRR comes entirely from FCF and you make slightly over 13%. With 4% growth, your IRR is close to 25%. Again, please note I’m using a constant 8.5x EBITDA multiple here. If Altice shows the ability to grow, the multiple is most likely coming up.

Given all of the free cash flow generation, unless the company seriously mis-allocates capital (hello Mint Mobile), the only way to really lose here on an absolute dollar basis is to see EBITDA dollars perpetually decline over time. In this scenario, some of the FCF will need to be allocated to leverage reduction as lower EBITDA leads to a higher debt / EBITDA ratio. If this happens, the fair value is much lower than the current multiple, and FCF/share will struggle to grow much. Paired with the leverage, the downside would be considerable.

What Results Can We Expect?

Now that we have a sense for how EBITDA growth (or a lack thereof) drives returns, what do we think we can realistically expect going forward?

Again, I find it helpful to break this discussion down between Optimum and Suddenlink:

For Optimum, over the past few years we’ve likely seen flat to slightly increasing penetration even as 60% of their network is inferior to its fiber competition. Given their own system upgrades, I find that assuming flat penetration going forward would be quite conservative.

We can layer on top of that an expectation for higher ARPU from both price increases and customers upgrading their speed. We can also expect slightly lower opex and capex per customer as most of the network is upgraded to fiber, which costs less to maintain.

With flat penetration, higher ARPU, and slightly reduced cost, 2% EBITDA growth should be easily achievable over the Optimum network.

For Suddenlink, from the prior section we know that we should have ~120k annual broadband additions per year over the next five years, which compares to current subscribers of ~1.7mm.

If Suddenlink is going to only grow EBITDA at 2% / year, they’re going to need to lose a pretty significant amount of broadband subscribers from their current footprint. It’s a little difficult to know what the cutoff point would be, given that hypothetical customer losses from their current system would be over a largely fixed cost base, but my guess is you might need to lose ~50k subscribers or more to limit total EBITDA growth to around 2%.

This would be a drop in broadband penetration of roughly 1.5 percentage points per year and a loss of ~3% of current subscribers annually. That would be an absolutely huge decrease in subscribers and unlike any kind of cable customer loss I’ve ever seen.

Given the above, I believe that Suddenlink can grow EBITDA by at least 2% / year, and likely quite a bit more than that, given the large increase in broadband subscribers from its edge-outs and upgrades. And remember, on top of subscriber gains, we should also have gains from price and mix similar to Optimum.

If we can get at least 2% annual EBITDA growth from each system, and I believe that we can, we should be able to make the high-teens or higher returns we’d need to clear our opportunity cost hurdle of CHTR / LBRDK.

Some More Risks

It’s important to go over some other risks to see what might be able to hurt us. Keep in mind from above that all we need to really lose here, given the leverage, is slightly negative EBITDA dollars over time.

More successful competition from fiber - Verizon has had a relatively strong past two years with its FIOS business. They seem to be competing better than they have historically. If they continue to succeed here, then flat penetration for Optimum could prove to be an aggressive assumption, even with plant upgrades. Separately, incremental fiber across the Spectrum footprint could prove to be tougher competition than expected, or it could provide something of a price ceiling for Suddenlink’s already high priced services.

5G home internet - I believe that 5G home internet will struggle to compete with cable given very real capacity constraints coupled with the fact that home broadband customers use orders of magnitude more bandwidth than wireless customers. However, Suddenlink’s footprint has relatively low population density, which is precisely where capacity constraints could be least onerous. 5G home internet could siphon off some broadband subscribers in those lower density areas.

Regulation - This is always a risk for any cable company. We haven’t seen any talk of price caps yet, but it is always a possibility, and Altice does charge high prices so it could be at relatively higher risk than other cable companies.

More FTTH build by Altice itself - Altice could decide to build more fiber over its footprint, perhaps building some in Suddenlink to defend its position against some of the above threats. That could lead to higher capex in the out years than I assume. The spend might come at okay returns, but that might be because without the spend results would deteriorate quickly.

Spurious M&A - I believe that Drahi is shrewd and wants to maximize his net worth over time, but I would be kidding myself if I thought it was impossible for him to try to empire build. He wouldn’t be the first cable executive to spend money in less attractive areas than his core business in an effort to diversify. The Mint Mobile deal wouldn’t make a lot of sense, but even if they buy Mint it would only lower the forward IRR by 1% / year or so. It would be more worrying if Drahi started to buy more assets on top of Mint that didn’t make sense.

These are all very real risks. Of course, nothing is risk free, but with significant leverage, investors need to be very attuned to all of these possibilities.

Conclusion

Altice is, admittedly, not my favorite cable company. I don’t love its high price / low service quality strategy. But cable is a hell of a good business, and Altice looks a bit better than it first appears - its FTTH build should help results in its Optimum footprint, and there’s a clear large growth path for Suddenlink via speed upgrades and new builds. These factors put together make it look to me like the odds are very good for EBITDA growth over time. When you pair that with a valuation that only demands ~2% EBITDA growth to make high-teens IRRs, Altice looks like a compelling long.

Very well done, good write-up here Kyler.

And even managed to take a shot at Comcast!

Great write up. I've been a long term CHTR/LBRDA holder, but your write up and current ATUS price may force me to rethink the risk/reward.